Cities, which house almost 60% of the world’s population are also responsible for two-thirds of the world’s energy consumption, and consequently emissions. Further, increased urbanisation trends means that the role of cities in tackling environmental and social issues will continue to grow. Urgent action is required by cities to address these global challenges locally.

Cities are the global centers of communication, commerce and culture. They are also a significant, and growing, source of energy consumption and greenhouse gas (GHG) emissions and produce more than 70% of the world’s emissions. A city’s ability to take effective action on mitigating climate change, and monitor progress, depends on having access to good quality data. Planning for climate action begins with developing a GHG inventory. An inventory enables cities to understand the emissions contribution of different activities in the community.

Environmental, Social, and Governance (ESG) is a framework used to assess the impact of an organisation on society and the sustainability of its investment across three central pillars. In the corporate sector, ESG assessments are a rapidly growing trend and investors now apply non-financial, sustainability and ethical considerations to drive investment decisions.

An environmental, social, governance (ESG) framework can offer a structured approach for cities and local governments to assess and address these socio-environmental challenges, while also ensuring good overarching governance. By adopting such an approach cities can also ensure their progressing towards the 17 United Nations Sustainable Development Goals, given their strong correlation. Smart and emerging technologies such as digital twins and blockchain can help city governments develop convenient solutions to their socio-environmental challenges.

In India, the key aspects of ESG have been traditionally covered under stand-alone laws such as the Environment (Protection) Act, 1986 and the Minimum Wages Act, 1948. However, over the last two decades, there have been a stream of reforms that have led to the inclusion of ESG in Indian organisations. The mandates for corporate social responsibility as well as business responsibility and sustainability reporting by SEBI are pivotal in building a culture for ESG.

| Era of Socially responsible Investing | • 1800s Socially Responsible Investing (SRI) with faith based organizations • 1960s-80s Emergence of modern SRI with movements for civil rights, women’s rights, |

| Recognition of Corporate Role in Sustainability | • 1992 Recognizing role of Financial Institutions in Sustainable Development Statement of Commitment by Financial Institutions on Sustainable Development issues by the UN Environment program (UNEP) • 2001. Emergence of CSR European Commission’s paper on “Promoting a European framework for Corporate Social Responsibility” • 2004 The term ESG first appears on UN Global Compact report on “Who Cares Wins – Connecting Financial Markets to a Changing World” • 2007 Sustainable Stock Exchange Initiative (SSEI) – peer-to-peer learning platform for exploring how exchanges can encourage sustainable investment • 2014 International Capital Market Association (ICMA) first published the Green Bond Principles2021 COP26 and Glasgow Climate Pact |

| Climate Change Conciousness | • 1992 Emerging movement on Climate Change Rio Earth Summit – United Nations Framework Convention on Climate Change (UNFCCC) • 1997 Kyoto Protocol– common language to communicate impacts by businesses and organizations • 2006 UN Principles of Responsible Investing (UN PRI) UN Environmental Program’s Finance Initiative’s (UNEP-FI) “Freshfield Report” These two reports form the basis of UN-PRI (Now with over 2400 signatories) at the New York Stock Exchange • 2015 COP21 and Paris AgreementTask Force on Climate Related Financial Disclosures (TCFD) established by the G20 – governance, strategy, risk management, and metrics and targets |

| ESG/Integrated Reporting Movement | • 2000 UN Global Compact • 1997 GRI – Global Reporting Initiative – common language to communicate impacts by businesses and organizations • 2022 Towards standardization of ESG Davos Manifesto 2020: – a set of 22 quantitative core metrics focus on objectives that are within a company’s own capabilities. • 2011 Sustainability Accounting Standards Board (SASB) to standardize sustainability accounting and measurements with standards that display both sustainability and financial fundamentals for outcomes • 2015 UNSDG Sustainability Goals • 2022 International Sustainability Standards Board established after converging International Integrated Reporting Council (IIRC 2009), SASB (2011), Climate Disclosure Standards Board (CDSB 2007), Value Reporting Foundation (2021) |

ESG in India – Timeline

- 2008 Launch of the ‘S&P ESG India Index’, first investable index of companies

- 2009 CSR guidelines by Ministry of Corporate

- 2011 National Voluntary Guidelines (NVGs) on CSR by Ministry of Corporate Affairs

- 2012 -SEBI mandated to file Business Responsibility Report (BRR) based on NVGs for top 100 listed companies

- 2013 MSCI India ESG leaders Index was introduced

- 2014 -CSR mandated with the Companies Act

- 2015 SEBI regulations to facilitate issuance of municipal bonds, BRR filing extended from 100 to 500 top listed companies ,Priority sector lending by banks for renewable energy and social infrastructure

- 2016 Green Bond guidelines, SEBI advised top 500 companies to adopt Integrated Reporting, required to prepare BRR on voluntary basis

- 2017 Kotak Committee on Corporate Governance,Green Bond disclosures

- 2018 Business Responsibility and Sustainability Reporting (BRSR) proposed

- 2019 National Guidelines on Responsible Business Conduct (NGRBC)

- 2021 Task Force on Sustainable Finance – NITI Aayog and the Ministry of Environment, Forests and Climate Change

- 2022 BRSR mandatory for top 1000 companies. Voluntary reporting for others with BRSR Lite Consultation paper by SEBI on ESG rating providers for the securities market

- 2023 SEBI mandates disclosure of BRSR Core, Transition scores, and ERP registration and certification. New category of ESG investing by Mutual Fund schemes and related disclosures

Globally, there is a momentum for reporting ESG in cities with the examples of Toronto rolling out a debt issuance programme linked for ESG outcomes.

There is an emerging market for ESG with municipalities in India as well. Rapid urbanisation, deteriorating environment and the state of municipal finances in India suggest that cities will need to reduce their dependence on grant funds and seek funds from the open market. In this scenario, ESG assessments become relevant to identify improvement opportunities and build credentials for attracting a diverse range of investors.

Fundraising through Municipal bonds has tripled in the last five years. The Government has also announced plans to raise US$2 billion to support green infrastructure projects through Sovereign Green Bonds. The Securities and Exchange Board of India (SEBI) requires that Municipal Governments obtain credit rating from at least one registered agency before issuance of municipal bond.

This need is further reflected in the trend of municipalities going for ISO certifications for various functions.

Indian municipalities with ISO certifications

- ISO 9001 for Quality management systems – Agra (City Admin), Bhubaneshwar (FSSM), Kavarapatti (Govt. School)

- ISO 14001 for Environmental management – Namakkal (Provision and Maintenance of Water Supply, Solid Waste/Sewage Management, Town Planning, Lighting)

- ISO 37120 for Sustainable cities and communities – Jamshedpur, Surat, Pune, Ahmedabad and Vijayawada (standardization of urban data)

This market presents an opportunity for Indian municipal authorities to link with a new source of capital that is focused on ESG outcomes. The recent municipal bond issue (Rs 150 crore) of Ghaziabad is the first municipal green bond issue and many more cities are likely to follow this path.

Cities are Already reporting on many indices and tracking national/ global commitments

Cities are mandated to provide many obligatory and discretionary functions spanning several ESG-related aspects. While data reporting across cities has not been uniform in the past in India, there is a significant shift towards increased collection of information on cities.

Indian cities have started to report on such aspects with the introduction of indices such as

- Ease of Living Index (EoL) and Municipal Performance Index (MPI),

- Climate Smart Cities Assessment Framework (CSCAF),

- Data Maturity Assessment Framework (DMAF)

- Swachh Survekshan.

- IT platforms such as Performance Assessment System (PAS) of CWAS,

- Open Government Data Platform,

- India Urban Data Exchange, etc. are also driven by the government.

Leveraging on the fact that cities are already reporting on various indices and a plethora of information/ data is available, an ESG framework for cities can be formulated as a tool to plan their investments around the environmental, social and governance fabric.

A key argument for ESG assessment at the city level is that cities provide many functions spanning several ESG-related aspects. These are listed in the Twelfth Schedule of the 74th Constitutional Amendment Act of 1992. However, the 18 functions listed under the 12th Schedule are suggestive in nature and it is the State Government’s decision to include them in respective municipal legislations.

Thus, many indicators used in the ESG framework may be under the purview of the state government, parastatal agencies, etc. Due to this, there are various indicators for which information is available only at district or state level. As mandates differ between cities in different states, the framework needs to be contextualised.

Additionally, diversities in geography and population size need to be considered. The ESG framework reported here provides a structured approach for cities, local governments, and investors to assess and address the challenges which the city faces irrespective of the institutional mandates.

74th Amendment and 12th Schedule

Power, authority and responsibilities of urban local governments –

- Urban planning including town planning

- Regulation of land-use and construction of buildings

- Planning for economic and social development

- Roads and bridges

- Water supply for domestic, industrial and commercial purposes

- Public health, sanitation conservancy and solid waste management

- Fire services

- Urban forestry, protection of the environment and promotion of ecological aspects

- Safeguarding the interests of weaker sections of society, including the physically and mentally disabled.

- Slum improvement and upgradation

- Urban poverty alleviation

- Provision of urban amenities and facilities such as parks, gardens, playgrounds

- Promotion of cultural, educational and aesthetic aspects

- Burials and burial grounds; cremations, cremation grounds; and electric crematoriums

- Cattle pounds; prevention of cruelty to animals

- Vital statistics include registration of births and deaths

- Public amenities including street lighting, parking lots, bus stops and public conveniences.

- Regulation of slaughterhouses and tanneries.

Organizations providing governing principles

- UNGC: UN Global Compact has ten principles. By adopting these, companies can uphold their basic responsibilities to people and planet.

- SDG: The Sustainable Development Goals (SDGs) or Global Goals are a collection of 17 interlinked global goals designed to be a “blueprint to achieve a better and more sustainable future for all “.

- UNPRI: Principles for Responsive Investment works with signatories to identify key environmental, social and governance issues in the market, and coordinates engagements, publications, webinars, podcasts, and events to address them.

- WB: World Bank – Sovereign ESG Data Framework incorporates data relevant to all 17 SDGs, which are crucial for financial sector representatives to consider when assessing the contribution of investments or policies to sustainable development.

Reporting frameworks

- GRI: The Global Reporting Initiative is an international, independent body that helps businesses, governments and other organizations understand, develop and communicate sustainability metrics. GRI relies on voluntary disclosure.

- SASB: The Sustainability Accounting Standards Board is a non-profit organization. It has developed a global standard for identifying, managing and communicating financially-material sustainability information to investors. This can be used in conjunction with other frameworks.

- TCFD: The Task Force on Climate-Related Financial Disclosures was created to improve and increase reporting of climate-related financial risks.

- CDP: The Carbon Disclosure Project is an international non-profit organization which helps companies and cities disclose their environmental impact.

- IIRC: International Integrated Reporting Council, established in 2010, framework with periodic integrated report by an organization about value creation over time and related communications regarding aspects of value creation.

- CDSB: The Climate Disclosure Standards Board is an international consortium of NGOs that are set to help organizations integrate information related to climate change in their financial reporting.

As per GRI Reporting framework GHG emissions from city activities shall be classified into six main sectors.

Sectors and sub-sectors

STATIONARY ENERGY

- Residential buildings

- Commercial and institutional buildings and facilities

- Manufacturing industries and construction

- Energy industries

- Agriculture, forestry, and fishing activities

- Non-specified sources

- Fugitive emissions from mining, processing, storage, and transportation of coal

- Fugitive emissions from oil and natural gas systems

TRANSPORTATION

- On-road

- Railways

- Waterborne navigation

- Aviation

- Off-road

- WASTE

- Solid waste disposal

- Biological treatment of waste

- Incineration and open burning

- Wastewater treatment and discharge

INDUSTRIAL PROCESSES AND PRODUCT USE (IPPU)

- Industrial processes

- Product use

AGRICULTURE, FORESTRY AND OTHER LAND USE (AFOLU)

- Livestock

- Land Aggregate sources and non-CO2 emission sources on land

Emissions Scope Definition

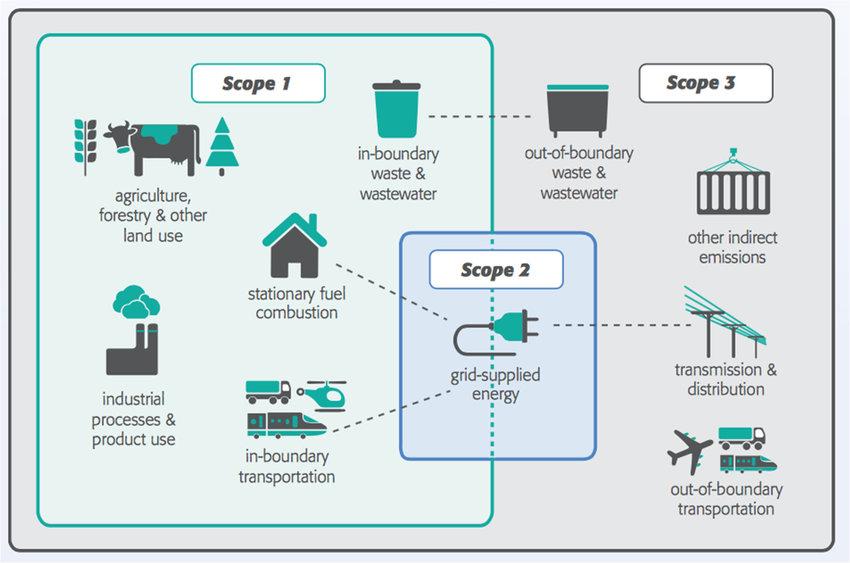

Scope 1 Emissions: GHG emissions from sources located within the city boundary

Scope 2 Emissions: GHG emissions occurring as a consequence of the use of grid-supplied electricity, heat, steam and/or cooling within the city boundary

Scope 3 Emissions: All other GHG emissions that occur outside the city boundary as a result of activities t taking place within the city boundary

ESG rating agencies

- MSCI: Morgan Stanley Capital International provides third party reports based on data from various sources.

- S&P: S&P Indices are designed to track the global green bond market, which maintains stringent standards to finance only environmentally friendly projects.

- ISS: Institutional Shareholder Services Inc. provides differentiated data, analytics, and insight to the institutional investor and corporate issuer communities.

- ESG Book: Makes sustainability data more widely available via digital platform, ESG information in realtime, and promotes transparency.

- EIU: Economist Intelligence Unit provides ESG rating service based on 90 indicators for 150 countries across the globe.

Rationale for ESG assessments for the City

Indian cities account for nearly two-third of the country’s GDP. Cities are increasingly seeking investment from capital market, private investors, and development finance institutions. In line with global trends, cities will need to prepare themselves for ESG assessments.

Already reporting on many indices and tracking national/ global commitments. Cities are mandated to provide many obligatory and discretionary functions spanning several ESG-related aspects. While data reporting across cities has not been uniform in the past in India, there is a significant shift towards increased collection of information on cities.

Indian cities have started to report on such aspects with the introduction of indices such as:

- Ease of Living Index (EoL)

- Municipal Performance Index (MPI),

- UNSDG – Sustainable Development Goals

- Climate Smart Cities Assessment Framework (CSCAF),

- Data Maturity Assessment Framework (DMAF) and

- Swachh Survekshan

- Pey Jal Sarvekshan

- Good Governance Index

- Mission LIFe

- Paris Agreement and Nationally determined Contributions

- IT platforms such as Performance Assessment System (PAS) of CWAS,

- Open Government Data Platform,

- India Urban Data Exchange, etc. are also driven by the government.

Leveraging on the fact that cities are already reporting on various indices and a plethora of information/ data is available, an ESG framework for cities can be formulated as a tool to plan their investments around the environmental, social and governance fabric.

At COP 26 in Glasgow, India made two significant commitments:

- Meeting 50% of energy needs from renewable fuels by 2030

- Transitioning to a net zero carbon economy by 2070.

At COP 27 in Egypt, India reiterated its updated Nationally Determined Contributions and the ethos around Mission LiFE. India is also committed to the SDGs. ESG framework provides a basis for meeting a large number of these global commitments at the city level

Driving Force for ESG Investments

India has the second largest urban population in the world with 11 percent of the total global urban population living in Indian cities (NITI Aayog, 2021).

Urban growth is expected to contribute to 73 percent of the total population increase by 2036 (MoHFW, 2019), further aggravating the pressure on a city’s infrastructure.

To meet the rising demand, a World Bank report estimates that India will need to invest US$840 billion over the next 15 years—or an average of US$55 billion per annum—into urban infrastructure if it is to effectively meet the needs of its fast-growing urban population. (World Bank, 2022).

Cities and parastatal agencies have two main sources of financing: own-source revenues and intergovernmental transfers.

Bridging the insufficient large infrastructure financing gap. A recent RBI report suggests that cities should explore different innovative bonds and land-based financing mechanisms to augment their resources. (RBI, 2022). The Union Budget 2022 talked about raising Rs.24,000 crore through Sovereign Green Bonds.

Sovereign Bondonomics:

- Municipal Bond:Debt instruments issued by municipalities or other state agencies which use the money for public good

- Green Bond: The proceeds of a Green Bond offering are ‘ear- marked’ for use towards financing ‘green’ projects

- Sustainability Bonds:Bonds where the use of proceeds will be exclusively applied to a combination of both social and green projects

- Blue Bonds: A debt instrument that is issued to support investments in healthy oceans and blue economies

- Social Bonds: Bonds where the use of proceeds is applied to raise funds for new or existing projects with positive social income

- Impact Bonds: A debt instrument to finance social services. In India, impact bonds have been successfully launched in the health and education sector

Municipal Bond Eligibility / Criteria as per SEBI:

- Credit rating from at least one third party credit rating agency registered with the Board

- The municipality should not have negative net worth for the last three financial years

- The municipality should not have defaulted in repayment of debt securities or loans

Few Investments made by Financial Institution/Banks for Cities

| 1 | Institutions | City/Municipalities Projects | ESG Purpose |

| 1 | World Bank (International Bank for Reconstruction and Development) | (International Bank for Reconstruction and Development) ▪ Ahmedabad City Resilience Project: The World Bank has committed US$ 280 Million to support the improvement of the institutional, financial and service delivery performance in Ahmedabad (World Bank, 2023d). ▪ Punjab Municipal Services Improvement Project: The World Bank provided a loan of US$ 105 Million to support the improvement of urban finances and governance, and sustainable watery service delivery in Amritsar and Ludhiana (World Bank, 2023e) | Environmental ▪ Quality of Water Supplied Social ▪ Coverage of WW network services ▪ Female labour force participation rate Governance ▪ Gender and Social Parity in Decision makers ▪ Own Revenue vs Total Revenue ▪ Extent of Cost Recovery in urban services |

| 2 | International Finance Corporation (IFC) | ▪ Lead transaction advisor to Bhubaneswar Municipal Corporation in a street-lighting network upgradation project (IFC & DevCo, 2020) ▪ Joint Venture with Tata Capital Limited to form Tata CleanTech Capital (leading green financier in India focusing on renewable energy and e-mobility), to which it issued a sustainability-linked bond of INR 3,750 million in 2023 (IFC, 2023e) | Environmental ▪ Air Quality Index Social ▪ Road Accident Fatality Rate |

| 3 | Asian Development Bank | ▪ Chennai Metro Rail Investment Project: Loan of US$780 Million (Asian Development Bank, 2023b) ▪ Supporting Access to Affordable Green Housing in Tier II and Tier III Cities for Women: Debt Security Financing of upto US$58,000,000 to IIFL Home Finance Limited (Asian Development bank, 2023c) ▪ Jharkhand Urban Water Supply Improvement Project: Loan of US$ 112 Million to improve treated piped water supply to Ranchi and three towns located in socio-economically backward areas (Asian Development Bank, 2021) | Environmental ▪ Availability of Public Transport ▪ Air Quality Index ▪ Green Buildings Adoption Social ▪ Economic Ability ▪ Percentage of houseless population |

| 4 | JICA (Japan International Cooperation Agency) | ▪ Kolkata East-West Metro Project: ODA Loan amount is 72,618 million yen and an additional loan of 25,903 million yen (through the President of India) to the Kolkata Metro Rail Corporation Limited (JICA, n.d.-b) ▪ Project for Construction of Chennai Seawater Desalination Plant (I): Total ODA Loan amount of 73.404 billion yen with 30 billion tranche 1 loan amount (Through the President of India) to Chennai Metropolitan Water Supply and Sewerage Board (JICA, n.d.-c) ▪ The Project for Implementation of Advanced Traffic Information and Management System in Core Bengaluru: Funding of Rs 72.86 crore (Belagere, 2018) | Environmental ▪ Availability of Public Transport ▪ Baseline Water Stress Social ▪ Smart systems deployed/ Integrated Command and Control Centre ▪ Road Accident Fatality Rate |

| 5 | Kreditanstalt für Wiederaufbau (KfW) | ▪ Funding towards Tamil Nadu Urban Development Fund: EUR 65 million loan with subsidised interest rates for projects in water supply, sewerage, and waste disposal and an IDA loan of EUR 10 Million for credit enhancement of pooled municipal bonds (German Missions in India, 2023) ▪ Climate-friendly metro system in Nagpur: Loan agreement of EUR 500 million towards city’s metro which is fueled mainly by solar energy (KfW, 2023b) | Environmental ▪ Various indicators under Water Resource Management ▪ Various indicators under Efficient Waste Management System ▪ Availability of Public Transport Social ▪ Various indicators under WASH services Governance ▪ Credit Rating Score of the ULB |

Way Forward for cities

Provision of basic services and amenities in cities require large investments. Currently, cities depend on central and state grant funds. However, cities will increasingly need to mobilize funds from the capital market, as suggested by a recent report of RBI on municipal finance.

Recent Government of India programmes such as AMRUT encourage cities to tap the capital market by providing incentives. At present, rating of bonds issued by cities is largely based on financial aspects. This attempt at developing an ESG framework for cities in India is not to develop yet another city ranking framework.

Aim should be to use publicly available information to develop ESG assessment or ESG rating of cities for demonstrating the larger role of our cities in achieving the broader goals related to environment, social and governance.